A few months after the Bank of England warned about AI’s soaring valuations, the Bank for International Settlements’ (BIS) latest observation –published earlier this month– is a call to investors and analysts to take note of new risks being embedded in the tech sector. AI is permanently changing Big Tech’s financial DNA.

The likes of Google, Microsoft, Apple, Meta, and Amazon have accumulated war chests to the tune of hundreds of billions of dollars. From the garage startups of the 1970s to the internet and cloud giants of the 2010s, the world’s most valuable companies built their empires on equity, venture capital, and their own prodigious cash generation. For over five decades, companies in Silicon Valley have operated according to an unwritten financial rule: technology companies don’t need debt.

However, this approach to capital structuring is changing, and changing fast. As a recently published BIS bulletin reveals, and cautions, technology companies are increasingly adding debt to their capital structures. This move is driven by the unrestrained pursuit of building a faster, better, deeper, and more capable system in the AI race.

The AI boom is forcing a fundamental restructuring of how technology companies finance themselves, marking the most significant shift in corporate finance since the LBO era of the 1980s. And unlike previous technological transitions, this one comes with new systemic risks that regulators, investors, and even the companies themselves may be vastly underestimating.

A quick catch-up on how things were: The old order

If we look back to the ‘70s and the ‘80s, we see that Silicon Valley in general and technology companies in particular have shunned the use of long-term debt. They did so with almost religious fervor. The reasons behind it are multifold, but we can look at three of them:

- Asset-Backed Anxiety: The foundation of traditional lending rests on a simple principle: if a borrower defaults, the lender seizes tangible assets—factories, equipment, real estate, inventory. These assets can be appraised, sold, and converted to cash with reasonable certainty. Banks have centuries of experience evaluating such collateral. Digital-age technology companies, however, broke from this approach. Their most valuable assets—source code, algorithms, patents, brand equity, network effects, customer relationships—are mostly intangible and are in the form of intellectual property rights (IPR). These assets present an insurmountable challenge to traditional lenders. Intellectual property is difficult to identify, impossible to separate from the business, and extraordinarily difficult to value objectively (assuming it is even possible to do so). Ergo, if a technology startup approached a bank for a loan, the bank viewed it as essentially an unsecured loan based on future cash flows from an unproven business model. Given this setup, traditional banks found it very difficult to lend to such businesses and, even if willing, demanded interest rates far higher than the founders imagined.

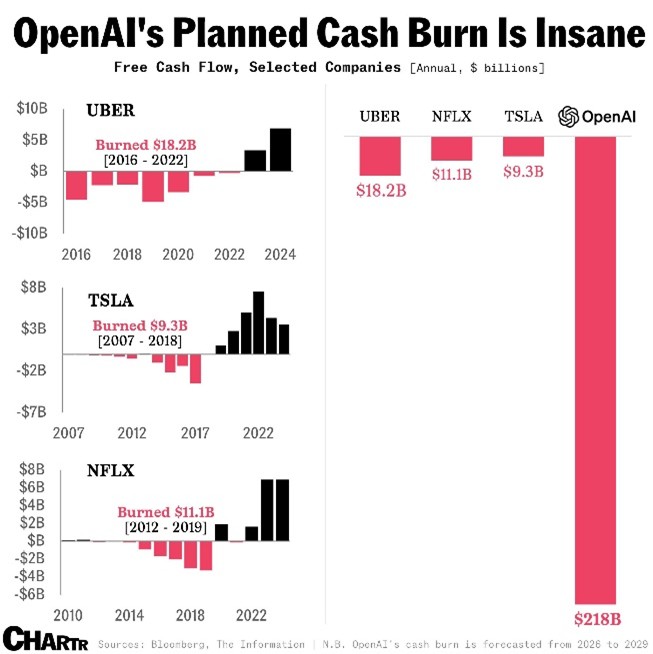

- The Burn Rate: The second most important constraint is the amount of cash technology startups need in the early stages of business. Instead of generating cash flows, they burn cash at an alarming rate. A typical VC-backed startup often spends years in negative cash flow territory, building products, acquiring customers, and establishing market position before achieving profitability. Companies like Uber, Tesla, and Netflix —which went on to become hugely successful in later stages–burnt billions of dollars in cash over several years before turning cash positive. Here’s a famous anecdote often attributed to Jeff Bezos when Amazon was burning cash at a frightening rate. By the late ‘90s, Amazon was losing money quickly and was being mocked by Wall Street analysts as a “sold a dollar for 90 cents” company. Banks did approach Amazon with structured debt offers. On paper, it made sense: predictable revenue growth, huge market potential, low interest rates. Bezos refused. He believed that debt creates fragility in a business model that is still in experimental stages. Bezos went on to say that those “interest margins are my opportunity to experiment.”

OpenAI cash burn Borrowing from banks requires companies to make regular interest payments at a minimum. These mandatory cash payments are often seen as an existential risk by the founders. After all, a company with negative operating cash flow and an uncertain revenue trajectory is hardly qualified to commit to making regular payments on the dot; one missed payment is all it takes to face default, the risk of bankruptcy, and the loss of control.

- Technology Opacity & Information Asymmetry: One of the lesser-known facets of technology startups is the degree of opacity they carry in their early stages. Silicon Valley founders have always been guarded about their IP —for very good reasons given the cutthroat competitive landscape in which they operate. However, it is just as likely that the founders and engineers have an in-depth understanding of the potential of their technology, the competitive landscape, and the probability of success far better than outside observers. When information asymmetry is high, lenders demand compensation through higher interest rates to protect against adverse selection —the risk that they’re lending to precisely those companies whose insiders know they’re likely to fail. This demand for higher interest payments again made the proposition unattractive. As equity investors, the venture capital (VC) community, on the other hand, developed expertise in technology evaluation and accepted the information asymmetry as part of their risk-return profile.

The Great Financial Crisis & the Tax Trap

The breakout of the Great Financial Crisis of 2008 seems to have permanently warped the global financial order. Not only did the “remedial policies” introduced to abate the crisis create a rupture between risk and return, but they also appear to have imparted a sense of disconnect between measures of (real) inflation and interest rates. Ever since central banks drove interest rates down to all-time lows, debt became extraordinarily cheap. Also, by then the bootstrapped tech companies from a few decades before —like Microsoft, Apple, Google, and others— had become massive, stable, cash-generating behemoths. They could easily procure investment-grade credit ratings given the amount of cash generated and their operating margins. Still, all of them shunned the use of debt for investments and operations; they just didn’t need it. They were already generating a lot more cash than they could productively invest. In particular, Apple was a notorious case in point at that time.

By 2013, Apple held nearly $145 billion in cash reserves, and about 70% of it was in offshore accounts (overseas). However, they could only remit these earnings back to the US at great cost. US tax laws mandated a 35% tax on foreign earnings when repatriated into the country, but the company owed nothing if those earnings remained overseas. Most of Apple’s cash was “trapped” by tax constraints. It couldn’t repatriate the money without paying tens of billions in tax. In the then-prevailing low-interest environment, Apple’s solution to this problem was elegant: a simple tax arbitrage. Apple decided to issue debt at under 3% p.a. in the domestic market and use the proceeds for shareholder returns while retaining the cash reserves in similarly low-yielding overseas accounts. Shortly after, Microsoft followed a similar strategy to reward its shareholders. (A few years later, the 2017 Tax Cuts and Jobs Act provided tax relief to companies looking to repatriate their earnings from overseas accounts.)

By the late 2010s, many of the tech companies –Google, Microsoft, Apple, Meta, Amazon, and others– had grown into mature businesses with a robust asset base, predictable revenues, investment-grade credit ratings, and massive scale. The subscription models offered by these companies only reinforced their financial stability in the long term. This maturation meant that the traditional arguments against debt —high business risk, negative cash flow, uncertain revenues— no longer applied to the top tier. They could access debt markets on favorable terms if they chose to. Despite this favorable congruence of factors, tech companies had limited debt exposure and only used it tactically, i.e., for tax purposes and maintaining credit market access. For the vast majority of the firms, all major capex and growth investments were funded using operational cash flows.

The AI Boom and its Inflection Point

With the breakout success of mainstream AI and the rise of LLMs, computer vision, multimodal models, etc., companies that were generating $50 to $100 billion in annual free cash flows suddenly felt they did not have enough cash to invest! Read that sentence again. The cash flows of these companies easily exceed the total revenue of many large companies —and even that was not enough for their AI ambitions.

The numbers surrounding the discussions concerning AI are staggering. Even more so when we talk about its financial aspects. For instance, Deloitte’s AI Infrastructure Survey shows that the largest eight hyperscalers invested about $371 billion in 2025 alone—which is more than 1% of US GDP and up 44% from the year before. The cumulative investment is expected to exceed $1 trillion within the next three years. These numbers are far higher than what happened during the dot-com boom, even in relative terms.

So, what makes AI so capital intensive?

a) Expensive Physical Infrastructure: Unlike a pure software operation, where products can be developed with modest levels of capital, AI requires extreme scales to offer a usable solution. Its physical infrastructure is a massive line item in the cost sheet. AI buildouts housing training clusters can span millions of square feet, consuming hundreds of megawatts of power. The industry rule of thumb is that data center equipment costs 3 times as much as the physical building itself. They are also immensely more power-hungry, with each rack designed for 60 to 90 kW —which is 4 to 6 times more compared to a traditional 10 to 15 kW rack.

b) Concentration and Urgency: The AI race has induced ubiquitous FOMO behavior among AI evangelists. Many executives sitting atop massive tech firms seem to have fallen prey to a “build now or fall behind forever” mentality. Companies fear that falling six months behind in AI capabilities could mean permanent competitive disadvantage. This urgency eliminates the option of pacing investments to match cash flow generation. This sense of urgency in pushing investments has negatively impacted the cost of construction materials, utilities, and even the price of RAM/Nand chips. Little thought is being given to the problem of stranded assets.

c) Power Grid Infrastructure: AI data center buildouts require electrical infrastructure on par with that of a small city. Adding to the cost are onsite and offsite disaster recovery systems and business continuity investments.

The BIS analysis starkly documents the fact that for the five major AI-investing firms (Amazon, Alphabet/Google, Meta, Microsoft, and Oracle), capex expense has surged in relation to their revenue. The FCF, in the aggregate, has also turned negative. Where will the remaining cash for the AI investments come from? Enter private credit.

A New Era of Tech Leverage: The Private Credit Revolution

The AI race has rewritten four decades of financial orthodoxy for the leading tech firms. The BIS report documents that private credit lending to AI-related sectors has grown from essentially zero to over $200 billion, representing nearly 8% of total private credit volumes. Projections suggest this could reach $300 to $600 billion by 2030, giving rise to concerns regarding new systemic risks regulators have to contend with.

From an AI company’s standpoint, one can see the attractiveness of using private credit: bespoke structures, faster approvals and fewer regulatory disclosures, and flexibility on the covenants away from public scrutiny. But more than any of that, AI companies are attracted to the potent combination of scale and speed. For instance, Bloomberg reports that the $3 trillion requirement in AI data center buildout projects has eclipsed the debt markets in general, and much of it is expected to come from private credit. Meta alone secured a $29 billion deal from PIMCO and Blue Owl Capital for a data center development —the kind of concentrated exposure that would be challenging in traditional syndicated bank markets.

For their part, private credit companies have successfully exploited the yield-seeking behavior of large pension funds, insurers, and other institutional investors by offering an illiquidity premium in exchange for tying up their capital for 6 to 8 years that happen to match the maturity profile of AI-infrastructure loans.

Key concerns noted in the BIS paper:

- The Valuation Disconnect: Among the various concerns raised in the BIS analysis, perhaps the most troubling one is the valuation disconnect. There is a wide chasm between how debt markets and equity markets are pricing AI risk. The BIS analysis notes that the loan spreads charged by private credit companies for AI investments are very similar to those charged for non-AI investments (ceteris paribus). In this case, 6.2% above benchmark rates for AI investments vs. 6.1% for non-AI firms. This pricing suggests that lenders view AI infrastructure investments as carrying roughly average risk for private credit borrowers.

They’re not demanding significant premiums for the technology risk, execution risk, or market risk inherent in AI investments. In contrast, the equity markets are telling a very different story. The report notes that the median forward P/E for AI-heavy companies stands at 31x, vs. 19x for the broader market. These valuations embed assumptions of extraordinary future growth and profitability. Investors are pricing in scenarios where AI generates transformative returns that justify premium valuations. This schism between the debt and equity markets exposes the dissonance in estimating the risk profile of the underlying AI assets. The report notes: “…either lenders may be underestimating the risks of AI investments (just as their exposures are growing significantly) or equity markets may be overestimating the future cash flows AI could generate.” Both possibilities are problematic.

If lenders are underpricing risk, the rapid growth of private credit exposure to AI infrastructure could create significant credit losses if AI investments disappoint. Given the scale and concentration of credit exposures in the market, these losses could materialize suddenly and surprise many actors. If equity markets are overvaluing AI companies, a correction could be severe, with spillover effects to credit markets as companies’ ability to refinance debt comes into question. The market capitalization of AI-related companies has grown so large that a significant correction would impact portfolio values globally. - The (In)visible Debt: Another point of concern noted in the BIS analysis is the presence of leasing agreements and off-balance-sheet financing arrangements among major AI players. Some AI infrastructure financing has moved off corporate balance sheets entirely through complex leasing arrangements and special purpose vehicles. These structures allow companies to access AI infrastructure without recognizing the associated debt on their primary financial statements, making leverage less visible to investors and regulators. As the BIS paper warns, “leverage does not disappear by being out of sight.” (Enron, anyone?) Market observers have raised concerns about the long-term value of collateral underpinning some large deals, questioning whether data centers will retain value if AI investment returns disappoint. As most people might be aware, there is little or no room to repurpose a data center for alternate use with comparable returns.

The Emerging Tech Capital Structure: A New Normal?

For several decades, software and technology companies have been asset-light —businesses mostly built on intellectual property, network effects, and relatively minimal physical infrastructure. While this model is still likely to be around in the years to come, things are changing at the very top. AI leaders are becoming capital-intensive businesses on par with traditional industrial companies. Microsoft’s annual capital expenditures now exceed those of many oil majors or automotive manufacturers. The distinction between “tech companies” and “capital-intensive companies” is blurring.

By looking at the way things are moving —and they are moving quickly— it seems that AI-focused companies will continue to generate the bulk of their cash flows from traditional software and services offerings, which will fund their operating expenses, new product development, and to a certain degree take care of their “internal” capex. However, considering the monumental scale of AI investments being considered, these companies are expected to take on additional debt to finance the AI infrastructure buildouts. These new data centers will likely be financed heavily using a mix of private and public debt, leases, SPVs, and off-balance-sheet arrangements.

Can it sustain?

So far, these companies have been quite successful in mobilizing cash to suit their needs. Will this gravy train continue? It probably will, for the most part, for the next few years. A more detailed answer depends on whether AI will deliver on its promises in the near future. As of now, most of the private credit extended to these companies matures between 2030 and 2032. If companies like OpenAI manage to conjure up a feasible revenue model —generating strong cash flows and justifying investments— refinancing should be straightforward as the asset class matures and the risk declines. For instance, would OpenAI’s first gadget—a speaker with a camera installed, connected to the ChatGPT engine and costing about $300—make an impact in the market? While cynics might wonder how different this would be from a standard smartphone with a tailored app installed on it, OpenAI is likely to insist that this product (and others like it) will pioneer a new category. Other rumored products include “smart glasses” like the ones made by Meta (and Google too, remember), and a smart lamp. After all, OpenAI spent over $6.5B last year to buy a hardware company that tinkers with AI-centered products and is expected to roll out more such devices. In the absence of a second “Project Stargate” being announced in 2029, AI companies’ ability to raise new cash will be contingent on how the market receives their offerings and how much it is willing to pay for them.

The Broader Question: Will AI Deliver

Listening to AI fanatics in Silicon Valley, one would be hypnotized into thinking that the current crop of AI and LLMs herald the advent of a new general-purpose technology on par with electricity, antibiotics, the internal combustion engine, or the internet. Such technologies reshape entire economies, creating productivity gains that justify enormous investment. Early evidence shows AI driving genuine productivity improvements in specific applications: software development, customer support, content creation, scientific research, and others. These gains are measurable and significant.

Skeptics, on the other hand, note that productivity gains from AI remain concentrated in narrow applications. Broader economic productivity data has not yet shown the transformative impact that would justify current investment levels. The circular financing arrangements and vendor lending in the AI ecosystem suggest some investment is driven more by capital availability and competitive pressure than by genuine demand for AI services.

Is this the biggest gamble in tech history?

For four decades, technology companies’ asset-light business models and strong cash generation insulated them from the leverage risks that have toppled companies throughout financial history. The AI boom is forcing them to abandon this insulation at the very moment when the returns on their investments are most uncertain.

The scale is breathtaking: hundreds of billions already committed, trillions projected over the next decade. The stakes are profound: AI could reshape economies and societies, or it could prove a costly detour that burdens companies with debt for years. The disconnect between debt market pricing and equity market valuations suggests profound disagreement about AI’s future. Lenders are treating AI infrastructure as just another moderately risky credit opportunity. Equity investors are pricing in transformative returns. Both cannot be right.

The BIS warning is worth heeding: “The long-term viability of the AI investment surge depends on meeting the high expectations embedded in those investments.” If those expectations are met, we’ll witness one of the great industrial transformations of the modern era. If they’re not, we may face a financial reckoning that reshapes both the technology industry and the broader economy. One thing is certain: the era of asset-light, self-financed technology companies has ended. Whatever emerges from the AI boom, the industry’s financial DNA has been permanently altered.

Written By — Prof. Abhijith S